Finally FAD happened. It was worth watching in its entirety.

During the Q & A, of course Lisa Su was asked about the effect of COVID-19 on Q1 and 2020. Amazingly she said AMD was not updating Q1 and 2020 remains the same! She did say that supply chain was nearly back to normal or normal in the next couple of weeks. Demand outside of China was good, and while there may be some weakness in China, but they also got some additionally sales in some 5G infrastructure projects (I am paraphrasing). They had guided for $1.8 B +/- 50 M, and if anything they are still within the lower range. This is much better than what people were expecting, since Microsoft had warned this week and Nvidia already warned to be short by $100 M.

There are several articles giving great coverage to this webcast.

AMD’s own press release, here.

TheStreet’s Eric Jhonsa covered it well, here.

AdoredTV did a great live blog, complete with slides, here.

ServetheHome did a nice run down on CDNA compute and 5 nm Epyc, here.

Finally Charlie Demerjian of SemiAccurate did a great technical overview, here.

Remember, FAD is all about long term financial model. Here are some of the notes I jotted down.

By 2023, AMD expects the TAM to be $79 B, including Data Center $35 B, PC $ 32 B (CPU and GPU), and Gaming $12 B.

AMD is introducing CDNA, specifically designed for GPU compute, optimized for HPC and machine learning, as opposed to the previously known RDNA, which is GPU for gaming. Nvidia has done this previously and Intel is doing it now. So this makes perfect sense. CDNA is for data center GPU compute, HPC and ML, all very sexy and currently dominated by Nvidia. This is great.

AMD is now promising significant free cash flow generation. Music to my ears.

Next comes the financial numbers.

Revenue growth at 20% CAGR.

Gross margin to be greater than 50 %.

CAPEX around 26-27%.

Operating margin to be mid-20s%.

Free cash flow to be >15% FCF margin.

Tax rate is currently 3% due to NOL , but will be 15% going forward.

From these numbers, one can start to calculate EPS for each subsequent years, keeping in mind that Lisa Su had traditionally guided conservatively, and had beaten the 2020 model quite handily.

AMD had sped up the design process by doing the following:

Leapfrogging teams.

Modular IP.

Design simulation to save time.

Hardware/software co-design.

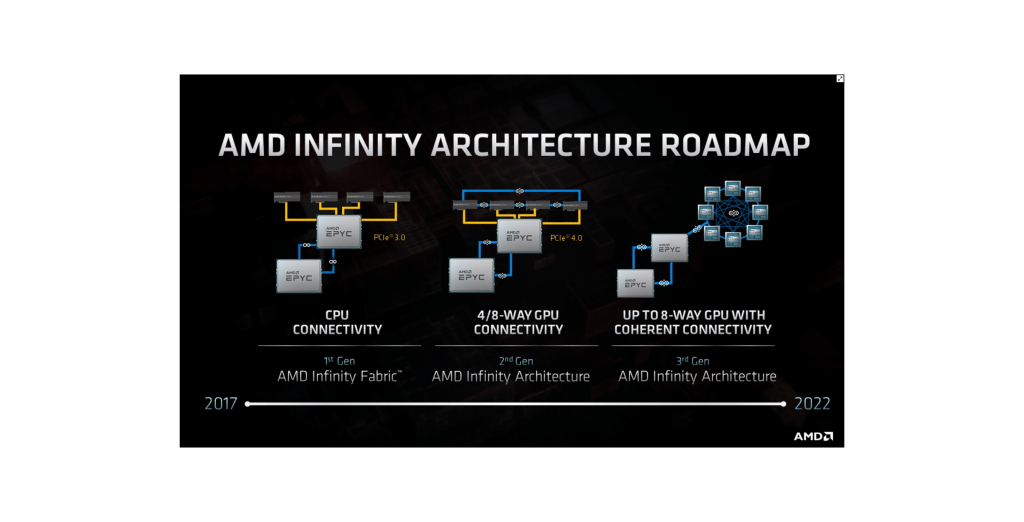

Next they talked about how important it is to have excellent CPU/GPU interconnect, and the 2nd and even 3rd generation Infinity Architecture (new term now). As a matter of fact, the advances in such interconnect is one reason AMD won the right to Frontier and El Capitan supercomputers. Another key concept is that of cache coherency, or essentially how well CPU and GPU talk to each other.

In other words, Infinity Architecture is great for great bandwidth, cache coherency and multi CPU and GPU interconnect.

Another tidbit, AMD had shipped 260 M Zen cores to date!

Security! AMD is promising even stronger security in the future.

RDNA2 has greatly increased performance per watt. RDNA was 50% over GCN, and now RDNA2 will be 50% over RDNA! Strong words indeed. It’s not all from the advance in process, but a lot of that improvement was from design/architecture.

AMD is coming with hardware accelerated ray tracing. Before, RT was not ready for prime time, where games were not offering it, and when used, tends to cause a performance hit. Here is looking at you, Nvidia.

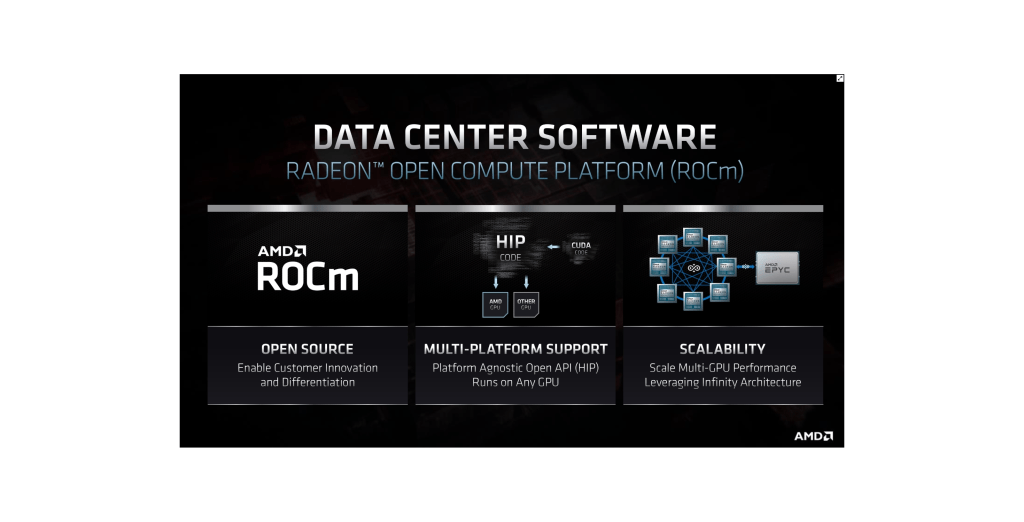

Software! ROCm, now version 4.0. Open source, multi platform, and highly scalable. Easy to port CUDA to HIP code. ROCm 4.0 is great for ML and HPC, and will be used for the exascale supercomputer! Remember that DOE is paying for software development, with $100M each for Frontier and El Capitan.

Another tidbit. AMD shipped 43 M units (for PC) in 2019. ASP went up by 14%. Market share in PC is up to 17% for 2019.

AMD’s new Renoir chips for notebooks can offer 18 hours of battery time.

Notebook share is already at 16% in 2019, before Renoir. Renoir has now 135 platforms for 2020 (was at 100 platforms when announced at CES 2020).

Navi 2X is promised for later this year, good for 4K resolution.

AMD reaffirmed double digit server share in Q2 2020.

Epyc Rome covered 80% of all server workloads, as in majority of cloud, all of HPC and significant usage for Enterprise IT. Now Milan can cover 100% of all server workloads. Epyc will have 140 OEM server platforms, up from 110 in 2019. Epyc cloud instances have increased from106 in 2019 to 150+ in 2020.

Server chips will account for 30% of total revenue, up from 15% in 2019. This will drive up the gross margin.

Also, there is packaging. AMD will be using X3D packaging, which is a hybrid between 2.5 and 3D. So AMD had gone from multichip module in 2017 to chiplets in 2019, and now will be continuing its innovation to X3D, promising 10X increase in bandwidth density.

Finally, AMD has talked about what do with all the free cash. There is talk suggesting share buyback or some other shareholder return vehicles. Then there is always the possibility of M&A.

I think all of these is enough for me to sleep very well for quite a while, through the COVID-19 crisis.