Intel Q2 earnings beat lowered guidance. The full year guidance was so so, with ever decreasing margin. However, the most damaging admission was that 7 nm chips will be delayed till 2022-23.

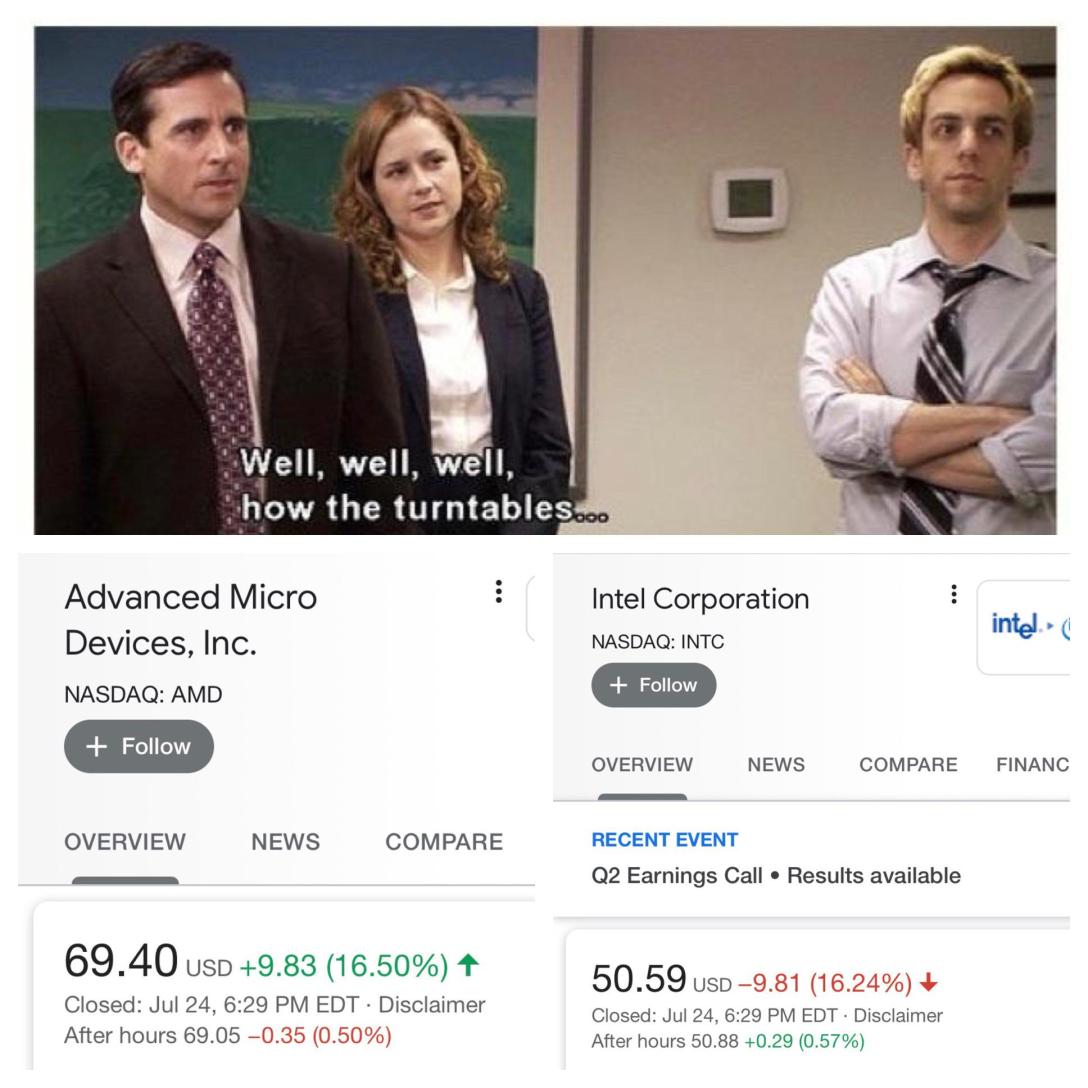

The market responded violently. INTC lost 15% of value, while AMD went up by 15% on Friday alone.

INTC ended up at 50.59, with 180 millions shares traded (average 25 millions shares) and AMD at 59.40, with 204 millions shares traded (average 59 millions shares)!

This is the beginning of a major trend reversal, paradigm shift of major magnitude. Institutional investors are starting to shift out of INTC, and into AMD, and not just in the next few days, but for the next few years.

More funds will be able to invest in AMD when AMD meets certain financial criteria, e. g. when AMD gets more credit rating upgrades (now sitting at Baa, one level below investment grade), when AMD achieves so many quarters of consecutive profit etc.

There is no need to go over the Intel’s entire saga of delays in 10 nm process. Intel has been putting up a brave front, pretending that their 7 nm is on track, and run by a separate team, etc. However, as TSMC had described, the advances made in each node are always transferred to the next node; so if Intel has trouble with their 10 nm process, in turn Intel will have issues with their 7 nm as well. Yet Intel had continued to mislead their customers in an effort to keep their business. Now with the road map pushed out three years, with likely further delays, there is absolutely no reason for OEMs and the big cloud players to stick with Intel.

Charlie Demerjian of SemiAccurate put out this excellent article on the Intel 7 nm timeline delay claims, here.

AdoredTV put out an excellent YouTube video concerning the Intel 7 nm disaster, here.

Certainly Intel can still sell their 14 nm+++++ chips and their 10 nm chips, but the fat margin will be gone. Also, AMD will continue to take market shares in all the segments.

Rome and Milan will do extremely well in the data centers.

Renoir mobile will do excellent business in the notebook segment, especially in the upcoming back to school season, with all the online classes being inevitable.

Renoir desktop APUs were announced on July 21. See AMD’s press release, here. Anandtech covered it, here.

Initially these APUs will be available only to OEMs, with sale to the DIY market few months later. Ryzen 3rd gen was already dominating the DIY desktop market since last summer. Now these Ryzen 4000 APUs will be most welcomed in the OEM desktop segment, where Intel had a monopoly. This is a segment where OEMs don’t want to mess with discrete GPUs. Now the Ryzen 4000 APUs can offer TSMC 7 nm process and up to eight cores, with excellent integrated graphics. Ryzen 4000 Pro chips will serve the business desktop segment. Finally AMD can compete in this playground, that of the OEM desktop.

Big Navi will arrive later this year for the consumer GPU market.

MI 100 will arrive soon for the data center GPU market.

Sony is rumored to increase PS5 initial order, up from 6 million units to 9-10 million units, per this TheVerge article.

Microsoft just hosted the Xbox Games Showcase event on July 23rd, as described by CNET, here.

In short AMD will meet or beat Q2 and should provide a great H2 guidance.

One final crucial point. Intel CEO Bob Swan prominently talked of Intel using outside foundry. As it is, Intel will use TSMC to make Ponte Vecchio data center GPU.

Demerjian wrote a great article on SemiAccurate.com, here.

Intel is unable to manufacture Ponte Vecchio in house, a key part of their Aurora exascale supercomputer. In order to avoid financial penalty and public humiliation, Intel is asking TSMC to make this GPU for them. However, it is important to note that this kind of outsourcing is low volume and will be limited.

Bob Swan had said the following gibberish:

“To the extent that we need to use somebody else’s process technology and we call those contingency plans, we will be prepared to do that,” Swan told analysts on a conference call, after the company warned of another delayed production process. “That gives us much more optionality and flexibility. So in the event there is a process slip, we can try something rather than make it all ourselves.”

Intel has foundries, and as such is a direct competitor to TSMC, just like Samsung. TSMC absolutely does not want to help its major competitor. TSMC serves fabless chip design companies, like Qualcomm, Apple, Nvidia and AMD. So the way Bob Swan is describing Intel’s on and off use of outside foundries, TSMC will be stupid to help Intel in any major capacity.

Furthermore, any wafer capacity TSMC can muster will be rapidly taken up by AMD, who is already TSMC’s biggest customer at 23%.

The only way for TSMC to serve Intel in a major manner in the future, is for Intel to become fabless. That is a very painful and difficult path for Intel.

MotleyFool put out this article on July 16 om AMD and TSM. Fittingly both stock had gained 30%+ in the last month.

meme credit goes to reddit user u/eat_a_plum.